Trade Info You Can Trust

CN 18-17, Provisional Safeguard Measures Imposed on the Importation of Certain Steel Goods

Customs Notice 18-17 provides additional information regarding the Notice to Importers, No. 911 issued on October 11. CN 18-17 should be read in conjunction with the Notice to Importers.

This Customs Notice describes a new surtax that does not apply to goods that originate in and are imported from the U.S., as well as other countries.

*****

Order Imposing a Surtax on the Importation of Certain Steel Goods:

- Steel plate

- Concrete reinforcing bar

- Energy tubular products

- Hot-rolled sheet

- Pre-painted steel

- Stainless steel wire

- Wire rod

1. This notice provides information on the implementation of the Order Imposing a Surtax on the Importation of Certain Steel Goods (the Order), registered on October 11, 2018 and which comes into force October 25, 2018.

2. The Order applies to certain steel goods (goods) imported from all countries except for the exclusions listed below:

- The Order does not apply to goods originating in and imported from the U.S., Chile, and Israel or another CIFTA beneficiary.

- For goods originating in and imported from Mexico, this Order only applies to energy tubular products and wire rod.

- Additionally, the Order does not apply to goods originating in and imported from developing countries which are beneficiaries to the General Preferential Tariff (GPT) with one exception: concrete reinforcing bar originating in and imported from Vietnam are not exempt. A list of GPT beneficiaries is included in Appendix A.

Note: Goods eligible for these exemptions must both originate in and be imported from the same country.

3. The origin of the goods is determined in accordance with the rules of origin set out in the Determination of Country of Origin for the Purposes of Marking Goods (NAFTA Countries) Regulations or the Determination of Country of Origin for the Purpose of Marking Goods (Non-NAFTA Countries) Regulations, as the case may be.

Application

4. Importers should refer to Schedule 1 of the Order to determine if the goods meet the product description of goods subject to the safeguard surtax.

5. Effective on the day on which the Order comes into force, a 25% safeguard surtax is applicable to imported goods that exceed the tariff rate quota (TRQ) for each class of goods set out in the Order.

6. Importers may request shipment-specific import permits (specific permits) from Global Affairs Canada, which will be valid for 14 days. Goods for which an importer obtained a specific permit, valid at the time of accounting, are exempt from the applicable safeguard surtax. Imports of goods that do not have a specific permit, or are in excess of the quantity of an import permit at the time of accounting, are subject to the safeguard surtax.

7. For information on conditions to satisfy when requesting specific permits, please refer to the Notice to Importers on Global Affairs Canada website. For general information about the permit application process and associated billing system, please refer to the Global Affairs Canada website: Import Controls and Import Permit.

8. The 25% safeguard surtax is applied on the value for duty of goods determined in accordance with sections 47 to 55 of the Customs Act.

9. Absent a specific permit, the safeguard surtax will apply to all goods including those released from a Customs Bonded Warehouse or Sufferance Warehouse on or after October 25, 2018 when the Order comes into force.

10. Canada’s Duties Relief Program and Duty Drawback Program continue to be available to importers for duties relief, including safeguard surtaxes, paid or owed by businesses that meet the requirements of these programs.

Proof of Origin/ Required Documentation

11. The burden of proof that goods do not originate from an applicable country as defined in the Order lies with the importer.

12. Proof of origin may be in the form of a commercial invoice, a Canada Customs Invoice, a Form A - Certificate of Origin, an Exporter's Statement of Origin, a Certificate of Origin pursuant to a Free Trade Agreement, or any other acceptable documentation that clearly indicates the country of origin of the goods.

13. To confirm whether imported goods are subject to the safeguard surtax, the CBSA may require importers to provide the following documentation:

- Specific permit

- Purchase invoice or order

- Bill of lading

- Mill certificate

- Product literature and technical specifications

- Any other document to substantiate whether the goods are subject to the safeguard surtax

Completing the B3-3 Canada Customs Coding Form

14. The following instructions and examples demonstrate how the B3 should be completed for importations of goods subject to provisional safeguards.

| Field | Instructions |

|---|---|

| 22 | Provide as much detail as possible. Where the goods are subject to provisional safeguards, state the specific product (steel plate, concrete reinforcing bar, energy tubular products, hot-rolled sheet, pre-painted steel, stainless steel wire, or wire rod). Where the goods are exempt, include information explaining why they are exempt. |

| 23 | Indicate the weight in kilograms. |

| 26 | Provide the specific permit number (number here is for illustrative purposes only) if applicable. If a permit has not been obtained leave blank. |

| 27 | Provide the goods’ 10 digit classification number. |

| 29 | For the quantity field, indicate the total weight of the goods. Use field 30 to indicate whether this is in kilograms or metric tonnes. |

| 30 | Specify unit of measure in kilograms (KGM) or metric tonnes (MT). |

| 32 | SIMA code 51 is used if the goods are subject to the safeguard surtax. SIMA Code 50 is used if a specific permit has been issued and the importation is exempt from the safeguard surtax. |

| 35 | GST rate is 5%. |

| 37 | Provide the value for duty of the imported goods in Canadian dollars. |

| 39 |

This field is used for both SIMA duties and the amount of safeguard surtax. The safeguard surtax is calculated at the value for duty (Field 37) x 25%. Where SIMA duties are also applicable, the SIMA duties and amount of safeguard surtax will be added together and entered in this field. |

| 41 | Value for tax = VFD + Safeguard surtax + SIMA duties (if applicable). |

| 42 | The GST is value for tax times 5%. |

Example 1: Safeguard surtax not payable (specific permit obtained) – no other applicable duties

- The specific permit number is entered in field 26.

- The SIMA Code (Field 32) is entered as 50, as the goods are exempt from the safeguard surtax.

Example 2: Safeguard Surtax payable – No other applicable duties

- No specific permit was obtained so the import is subject to the safeguard surtax.

- The SIMA Code (Field 32) is entered as 51, as the safeguard surtax is payable.

- The amount of safeguard surtax is calculated as follows: $44,200.00 (VFD) x 0.25 (25% safeguard surtax) = $11,050.00 (safeguard surtax payable).

- The value for tax is $44,200.00 (VFD) + $11,050.00 (safeguard surtax) = $55,250.00

Example 3: Safeguard Surtax payable in addition to SIMA duties

- The SIMA Code (Field 32) is entered as 51, as the safeguard surtax is payable.

- The amount of the safeguard surtax is: $44,200.00 (VFD) x 0.25 (25% safeguard surtax) = $11,050.00 (safeguard surtax payable).

- For this example, there are $2000.00 in SIMA duties.

- Amount to enter in Field 39: $11,050.00 (safeguard surtax) + $2000.00 (SIMA duties) = $13,050.00.

- The value for tax is $44,200.00 (VFD) + $11,050.00 (amount of safeguard surtax) + 2000.00 (SIMA duties) = $57,250.00

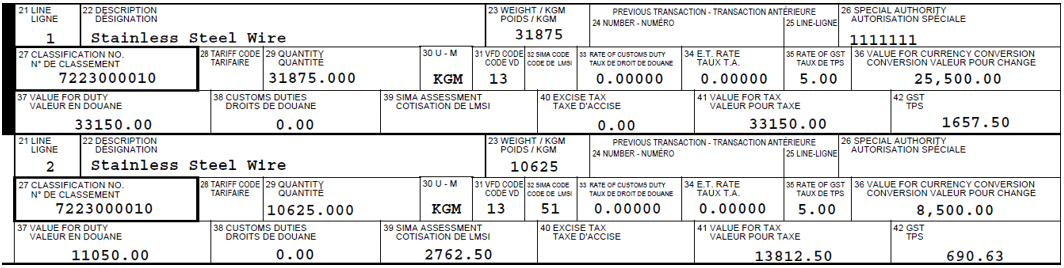

Example 4: Safeguard Surtax partially payable (specific permit obtained but part of importation exceeds TRQ)

- Where the quantity of imported goods exceeds the corresponding quantity of a specific permit, and the safeguard surtax is applicable to the exceeding quantity of goods, two lines need be completed as per Example 4: Line 1 where the goods are covered by a specific permit; Line 2 where the goods are not covered by a specific permit and subject to the safeguard surtax

15. For further information on the applicability of SIMA (anti-dumping) duties see the SIMA website, Measures in Force section.

16. Refer to Memorandum D17-1-10, Coding of Customs Accounting Documents for additional information on completing Form B3-3.

Corrections, Re-Determinations, and Refunds

17. Corrections to original declarations and requests for re-determinations or further re-determinations, and applications for a refund are to be made in the prescribed form and manner under the relevant provisions of the Customs Act, in accordance with the procedures outlined in Memorandum D11-6-7, as well as Memorandum D11-6-6, “Reason to Believe” and Self-Adjustments to Declarations of Origin, Tariff Classification, and Value for Duty, and Memorandum D6-2-3, Refund of Duties.

18. Where an overpayment of safeguard surtax has been identified on a commercial importation, Form B2, Canada Customs – Adjustment Request may be filed in a regional CBSA office requesting a refund of the overpaid amount under section 74(1)(g) of the Customs Act. If accounting information is being self-adjusted for a safeguard surtax refund or safeguard surtax payable to the CBSA, refer to Memorandum D17-2-1, The Coding, Submission and Processing of Form B2 Canada Customs Adjustment Request, for additional information on completing Form B2. Note that Customs Self Assessment (CSA) clients must use this process when seeking an adjustment of the safeguard surtax.

19. Refund requests for overpayments of SIMA duties must be filed on a separate B2 form. For more information on SIMA redeterminations, refer to Memorandum D14-1-3, Re-determinations and Appeals Under the Special Import Measures Act.

20. Accounting documents are reviewed by the CBSA to ensure that the correct amount of safeguard surtax was self-assessed by the importer. The CBSA may review the origin, tariff classification, value for duty and/or applicability of the safeguard surtax or SIMA duties on its own initiative or in response to a correction. In so doing, as with customs duties and taxes, the CBSA may assess any undeclared amount of safeguard surtax.

21. Decisions made by the CBSA may be subject to appeal under the Customs Act.

Examinations and Verifications

22. Importations may be subject to examination at the time of accounting and to post-release verification for compliance with the Tariff Classification, Valuation, Origin and Marking programs, and any other applicable provisions administered by the CBSA. If non-compliance is encountered by the CBSA, the safeguard surtax, SIMA duties and taxes, as well as penalties and interest will be assessed, where applicable.

Additional Information

23. Refer to Memorandum D16-1-1, Information pertaining to the application, collection, and adjustment of a surtax, for additional information concerning the administration and enforcement of safeguard surtax orders under sections 53(2), 55(1), 60, 63(1), 68(1), 77.1(2), or 77.6(2) or 78(1) of the Customs Tariff.

24. For more information on the administration of the safeguard surtax orders, within Canada call the Border Information Service at 1-800-461-9999. From outside Canada call 204-983-3500 or 506-636-5064. Long distance charges will apply. Agents are available Monday to Friday (08:00 – 16:00 local time / except holidays). TTY is also available within Canada: 1-866-335-3237.

Appendix A

| 1 | Afghanistan | 37 | Gambia | 73 | Paraguay |

| 2 | Angola | 38 | Georgia | 74 | Philippines |

| 3 | Anguilla | 39 | Ghana | 75 | Pitcairn |

| 4 | Armenia | 40 | Guatemala | 76 | Rwanda |

| 5 | Ascension Island | 41 | Guinea | 77 | Saint Helena and Dependencies |

| 6 | Bangladesh | 42 | Guinea-Bissau | 78 | Samoa |

| 7 | Belize | 43 | Guyana | 79 | Sao Tome and Principe |

| 8 | Benin | 44 | Haiti | 80 | Senegal |

| 9 | Bhutan | 45 | Honduras | 81 | Sierra Leone |

| 10 | Bolivia | 46 | Iraq | 82 | Solomon Islands |

| 11 | British Indian Ocean Territory | 47 | Kenya | 83 | Somalia |

| 12 | Burkina Faso | 48 | Kiribati | 84 | South Sudan |

| 13 | Burma | 49 | Kyrgyzstan | 85 | Sri Lanka |

| 14 | Burundi | 50 | Laos | 86 | Sudan |

| 15 | Cambodia | 51 | Lesotho | 87 | Swaziland |

| 16 | Cameroon | 52 | Liberia | 88 | Syria |

| 17 | Canary Islands | 53 | Madagascar | 89 | Tajikistan |

| 18 | Cape Verde | 54 | Malawi | 90 | Tanzania |

| 19 | Central African Republic | 55 | Mali | 91 | Timor-Leste |

| 20 | Ceuta and Melilla | 56 | Marshall Islands | 92 | Togo |

| 21 | Chad | 57 | Mauritania | 93 | Tokelau Islands |

| 22 | Christmas Island | 58 | Micronesia | 94 | Tonga |

| 23 | Cocos (Keeling) Islands | 59 | Moldova | 95 | Tristan Da Cunha |

| 24 | Comoros | 60 | Mongolia | 96 | Turkmenistan |

| 25 | Congo | 61 | Montserrat | 97 | Tuvalu |

| 26 | Cook Islands | 62 | Morocco | 98 | Uganda |

| 27 | Côte d'Ivoire | 63 | Mozambique | 99 | Ukraine |

| 28 | Democratic Republic of Congo | 64 | Naura | 100 | Uzbekistan |

| 29 | Djibouti | 65 | Nepal | 101 | Vanuatu |

| 30 | Egypt | 66 | Nicaragua | 102 | Vietnam* |

| 31 | El Salvador | 67 | Niger | 103 | Virgin Islands, British |

| 32 | Eritrea | 68 | Nigeria | 104 | Yemen |

| 33 | Ethiopia | 69 | Niue | 105 | Zambia |

| 34 | Falkland Islands | 70 | Norfolk Island | 106 | Zimbabwe |

| 35 | Fiji | 71 | Pakistan | ||

| 36 | French Southern and Antarctic Territories |

72 | Papua New Guinea | ||

|

Source: Canada Border Services Agency, Customs Tariff 2018 – List of Countries and Applicable Tariff Treatments * The safeguard surtax is applicable to imports of concrete reinforcing bar originating in or imported from Vietnam. This notice is also available on the CBSA website. |

|||||